If the lending institution takes your home in a foreclosure, you'll also lose any cash already paid up to that point. Any home you acquire can decline gradually. If the realty market drops and your home declines, you could end up with a home loan balance greater than the worth of your home.

The great news is the number of house owners having this issue has fallen dramatically, as house prices have actually continued to recuperate and headed back to their earlier highs. Purchasing a home might be the biggest purchase of your life, so it's a great idea to know the list below aspects prior to you start shopping.

The better your score, the lower your rate will likely be and the less you'll pay in interest. You're entitled to complimentary credit reports each year from the 3 major credit bureaus, so request them from annualcreditreport.com and dispute any mistakes that might be dragging your rating down. Lenders will more than happy to tell you how much they want to provide you, but that's not in fact a good indicator of just how much home you can manage.

Keep in mind that your regular monthly payment will be more than simply primary and interest. It will also consist of house owner's insurance, property taxes and, potentially, home loan insurance coverage (depending upon your loan program and deposit). You'll also need to consider energies and upkeep. If you receive an FHA, VA or USDA loan, you might have the ability to get a much better deal on rates of interest and other expenses utilizing their programs.

Whether you select a government-backed or traditional loan, charges and rate of interest can vary extensively by lender, even for the very same type of loan, so go shopping around for your best deal. You can start your search by comparing rates with LendingTree. Your credit history is an essential factor lending institutions consider when you're obtaining a mortgage, but bad credit won't always prevent you from getting a home loan.

Some Known Details About Understanding How Mortgages Work

You may have heard that you should put 20% down when you acquire a home. It holds true that having a big down payment makes it much easier to get a home mortgage and may even reduce your rate of interest, however many people have a difficult time scraping together a down payment that large.

Standard loan providers now offer 3% down programs, FHA loans provide down payments as low as 3.5%, and VA and USDA loans may require no down payment at all. The mortgage prequalification procedure can offer you a concept of just how much lenders might be willing to loan you, based upon your credit score, financial obligation and income.

As soon as you discover a home and make an offer, the lending institution will ask for additional documents, which might consist of bank statements, W-2s, tax returns and more. That procedure will figure out whether your loan gets complete approval. If you have concerns that it may be difficult for you to get approved, you might ask your loan officer whether you can get a complete credit approval prior to you start taking a look at houses.

There are a number of important elements of a loan that you need to know before you get going shopping. Closing expenses are costs over and above the sales price of a house. They may consist of origination costs, points, appraisal and title charges, title insurance, surveys, tape-recording charges and more. While charges differ commonly by the type of mortgage you get and by area, they usually total 2% to 5% of the house's purchase rate.

Money paid to your loan provider in exchange for a lower rates of interest. The cost of borrowing money, based upon the interest, fees and loan term, revealed as an annual rate. https://www.inhersight.com/companies/best/industry/finance APR was produced to make it much easier for consumers to compare loans with various interest rates and costs and federal law requires it be divulged in all advertising. how do mortgages work in the us.

The Facts About What Can Itin Numbers Work For Home Mortgages In California Uncovered

If you fall on tough times, it's important you understand the timeline and processes for for how long a foreclosure will take. The most essential thing to comprehend about judicial foreclosure is that it's a procedure that will go through the courts, and typically takes a lot longer with more expenses included.

If you signed a note and a deed of trust at your closing, then you are most likely in a state that permits a non-judicial foreclosure procedure. The courts are not associated with this process, and the foreclosure process can be much faster, leaving you with less time to make alternative housing arrangements if you are not able to bring the payments present.

However very few people invest as much time comprehending how a home mortgage really works. Besides informing you the regards to your loan, the home loan and deed of trust (if applicable) describe the rights your lending institution has to take ownership of your house if you are not able to pay. If you fall on difficult times, your first phone call must be to the company you are making payments to, called a mortgage servicer.

There are very rigorous laws that were passed in current years that require lenders do their due diligence to provide you all the choices possible to bring your home loan present or exit homeownership with dignity. By comprehending how your mortgage works, you can protect your investment in your home, and will know what actions to take if you ever have challenges making the payments.

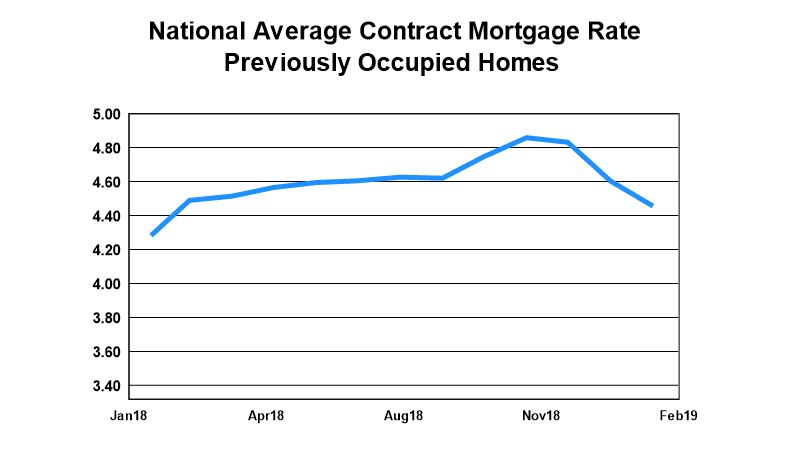

4 October 2001, Modified November 11, 2004, November 24, 2006, August 27, 2011, Rewritten September 17, 2016 The largest monetary deal most house owners carry out is their home mortgage, yet extremely couple of completely understand how mortgages are priced. The main component of the rate is the home mortgage rates of interest, and it is the only component debtors have to pay from the day their loan is paid https://www.inhersight.com/companies/best/reviews/telecommute?_n=112289508 out to the day it is totally paid back.

4 Easy Facts About How Do Assumable Mortgages Work Shown

The rates of interest is used to compute the interest payment the debtor owes the lending institution. The rates estimated by lending institutions are annual rates. On many home mortgages, the interest payment is determined monthly. Thus, the rate is divided by 12 before computing the payment. Consider a 3% rate on a $100,000 loan.

Multiply.0025 times $100,000 and you get $250 as the month-to-month interest payment. Interest is just one part of the expense of a mortgage to the customer. They also pay two kinds of in advance fees, one mentioned in dollars that cover the costs of particular services such as title insurance coverage, and one specified as a percent of the loan quantity which is called "points".

Whenever you see a home loan rate of interest, you are likely also to see an APR, which is practically always a bit greater than the rate. The APR is the home mortgage rate of interest adapted to consist of all the other loan charges mentioned in the paragraph above. The estimation presumes that the other charges are spread uniformly over the life of the mortgage, which imparts a downward bias to the APR on any loan that will be completely paid back before term which is many of them.